Show me the money: Tracking the companies that have a lock on sending funds to incarcerated people

Transcription

https://www.prisonpolicy.org/blog/2021/11/09/moneytransfers/

Show me the money: Tracking the companies that have a lock on sending funds to incarcerated people

We looked at all fifty state departments of corrections to figure out which companies hold the contracts to provide money-transfer services and what the fees are to use these services.

by Stephen Raher and Tiana Herring, November 9, 2021

As people in prison are increasingly expected to pay for everyday costs (food, hygiene items, correspondence, etc.), the mechanics of how people send money to incarcerated people assumes heightened importance. Family members used to mail a money order to a PO box, and a day or two later, the money would be in the recipient’s trust account. In those days, the most common complaint from family members and incarcerated recipients used to be about delays in processing money orders. Quick to use consumer psychology to turn a buck, a whole industry arose to provide faster–but vastly more expensive–electronic money transfers to incarcerated people.

This “correctional banking” industry includes specialized services like release cards, but at its core the industry makes money off the simple (but highly lucrative) business of facilitating transfers from friends and family members to incarcerated recipients. The industry relentlessly crows about the speed of electronic transfers, while conveniently glossing over the high fees that typically accompany these services. To get a better sense of the landscape, we looked at all fifty state departments of corrections and tried to figure out which companies (if any) hold the contract(s) to provide money-transfer services for each prison system. When possible, we tried to figure out what the fees are to use these services.

Below, we provide the results of our review, identify notable trends in this realm, and highlight steps families of people who are incarcerated, regulators, procurement officials, and companies can take to make money transfers more convenient, affordable, and easy to understand.

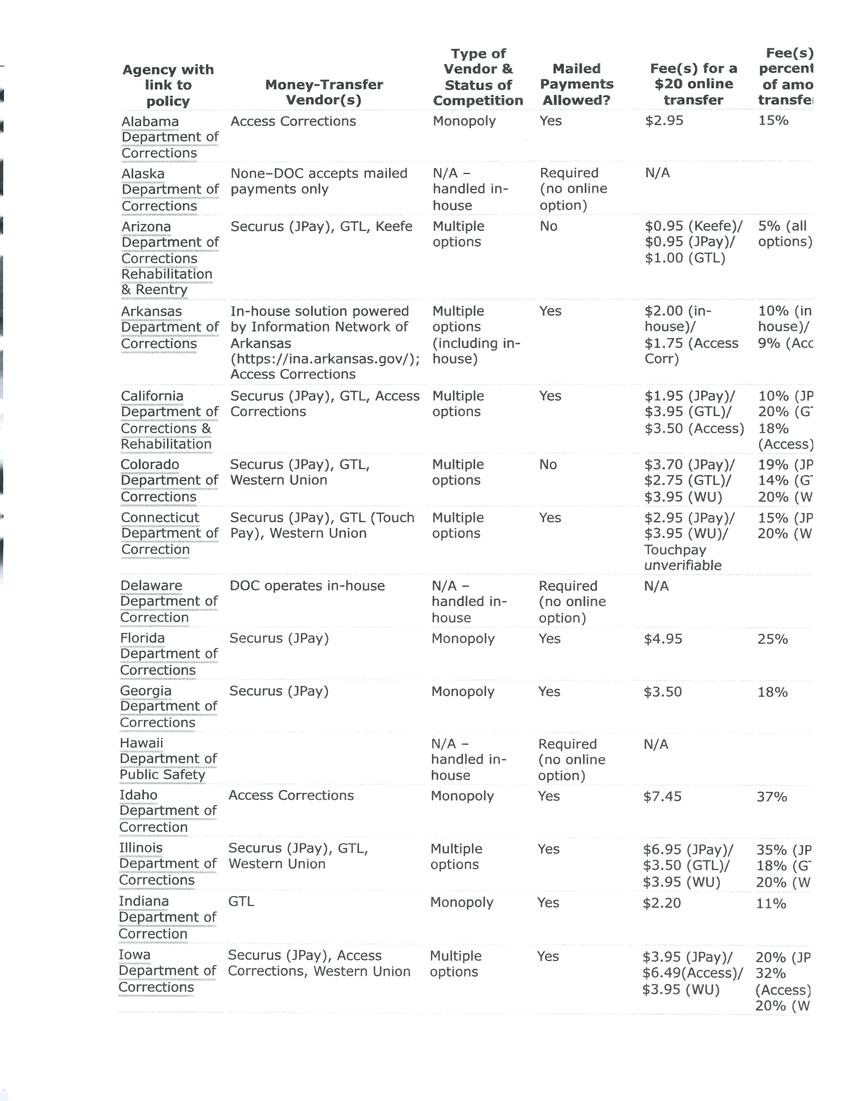

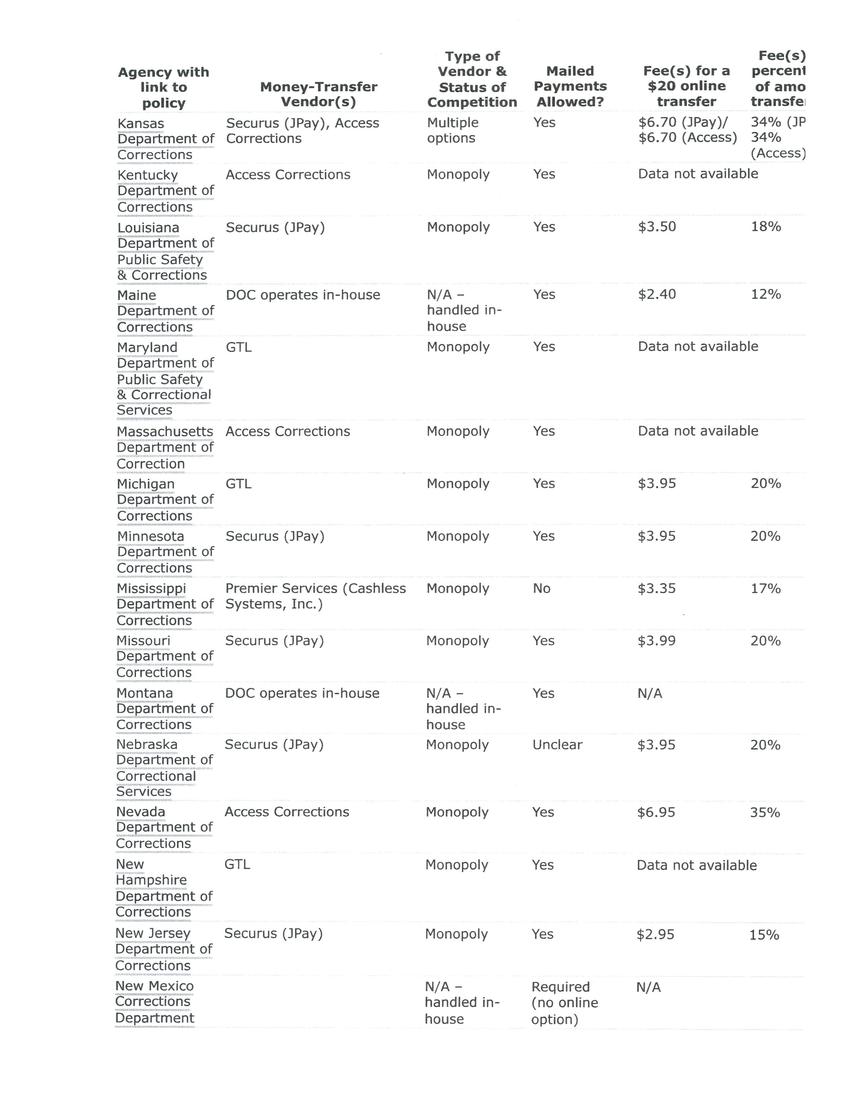

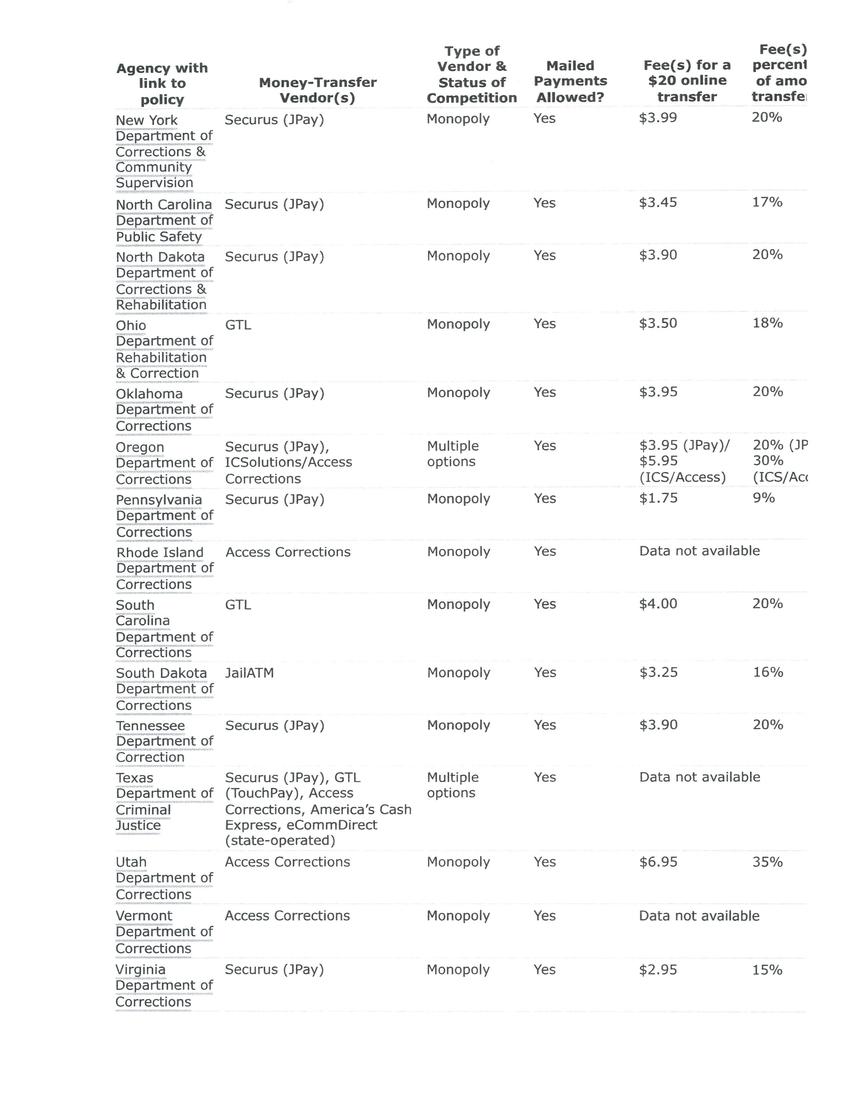

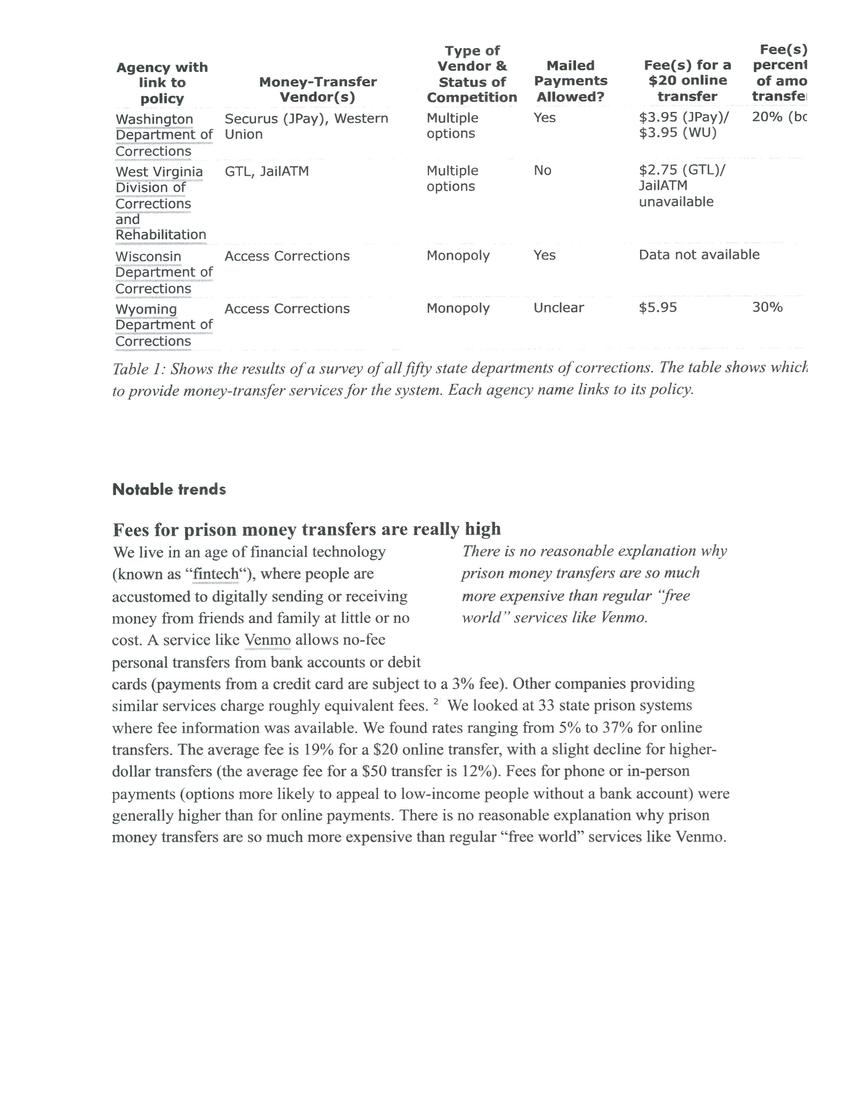

Table 1: Shows the results of a survey of all fifty state departments of corrections. The table shows which companies (if any) hold the contract(s) to provide money-transfer services for the system. Each agency name links to its policy.

Agency with link to policy Money-Transfer Vendor(s) Type of Vendor & Status of Competition Mailed Payments Allowed? Fee(s) for a $20 online transfer Fee(s) as percentage of amount transferred Fee(s) for a $50 online transfer Fee(s) as percentage of amount transferred

Alabama Department of Corrections Access Corrections Monopoly Yes $2.95 15% $5.95 12%

Alaska Department of Corrections None–DOC accepts mailed payments only N/A – handled in-house Required (no online option) N/A N/A

Arizona Department of Corrections Rehabilitation & Reentry Securus (JPay), GTL, Keefe Multiple options No $0.95 (Keefe)/

$0.95 (JPay)/

$1.00 (GTL) 5% (all options) $5.95 (Keefe)/

$5.95 (JPay)/

$4.95 (GTL) 12% (Keefe)/

12% (JPay)/

10% (GTL)

Arkansas Department of Corrections In-house solution powered by Information Network of Arkansas (https://ina.arkansas.gov/); Access Corrections Multiple options (including in-house) Yes $2.00 (in-house)/

$1.75 (Access Corr) 10% (in-house)/

9% (Access) $3.00 (in-house)/

$2.75 (Access Corr) 6% (both)

⇡

Show all states

⇣

Wyoming Department of Corrections Access Corrections Monopoly Unclear $5.95 30% $5.95 12%

Notable trends

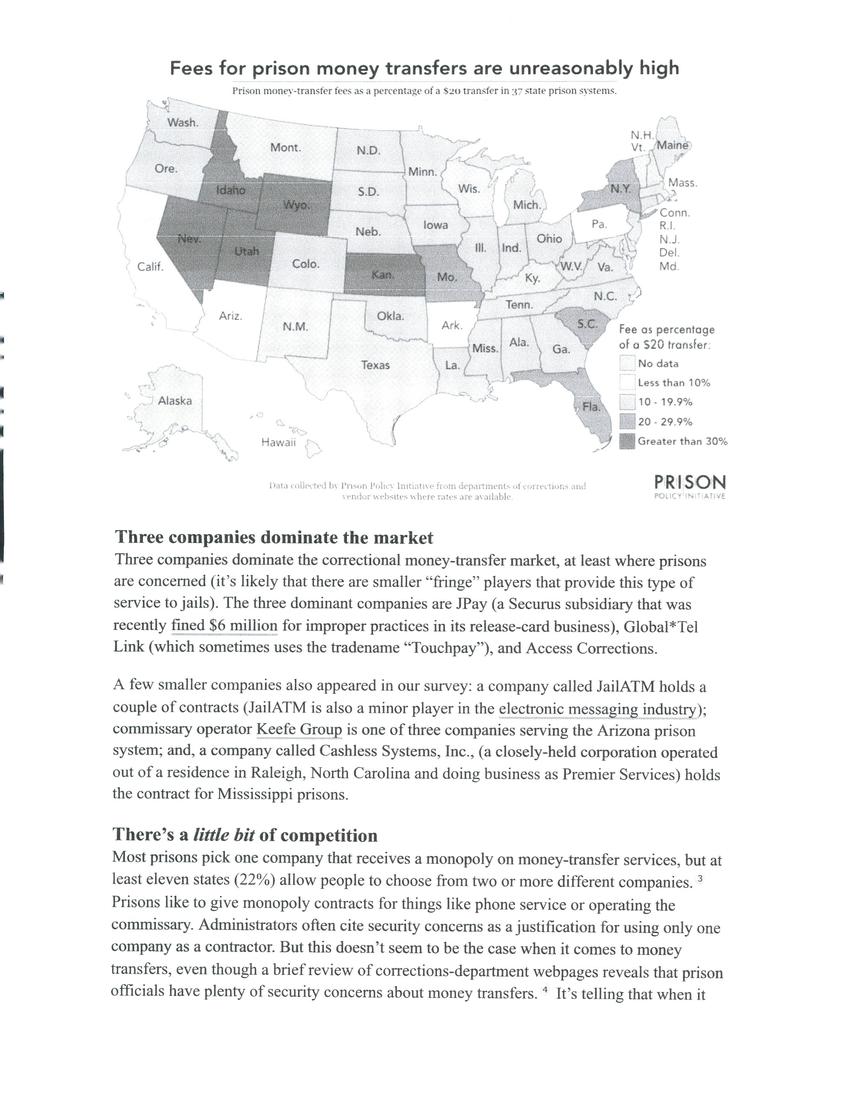

Fees for prison money transfers are really high

There is no reasonable explanation why prison money transfers are so much more expensive than regular “free world” services like Venmo.

We live in an age of financial technology (known as “fintech“), where people are accustomed to digitally sending or receiving money from friends and family at little or no cost. A service like Venmo allows no-fee personal transfers from bank accounts or debit cards (payments from a credit card are subject to a 3% fee). Other companies providing similar services charge roughly equivalent fees. We looked at 33 state prison systems where fee information was available. We found rates ranging from 5% to 37% for online transfers. The average fee is 19% for a $20 online transfer, with a slight decline for higher-dollar transfers (the average fee for a $50 transfer is 12%). Fees for phone or in-person payments (options more likely to appeal to low-income people without a bank account) were generally higher than for online payments. There is no reasonable explanation why prison money transfers are so much more expensive than regular “free world” services like Venmo.

A map showing fees for money transfers are unreasonably high

Three companies dominate the market

Three companies dominate the correctional money-transfer market, at least where prisons are concerned (it’s likely that there are smaller “fringe” players that provide this type of service to jails). The three dominant companies are JPay (a Securus subsidiary that was recently fined $6 million for improper practices in its release-card business), Global*Tel Link (which sometimes uses the tradename “Touchpay”), and Access Corrections.

money icon

SEARCH CONTRACTS

See the companies profiting off money transfers

A few smaller companies also appeared in our survey: a company called JailATM holds a couple of contracts (JailATM is also a minor player in the electronic messaging industry); commissary operator Keefe Group is one of three companies serving the Arizona prison system; and, a company called Cashless Systems, Inc., (a closely-held corporation operated out of a residence in Raleigh, North Carolina and doing business as Premier Services) holds the contract for Mississippi prisons.

There’s a little bit of competition

Most prisons pick one company that receives a monopoly on money-transfer services, but at least eleven states (22%) allow people to choose from two or more different companies. Prisons like to give monopoly contracts for things like phone service or operating the commissary. Administrators often cite security concerns as a justification for using only one company as a contractor. But this doesn’t seem to be the case when it comes to money transfers, even though a brief review of corrections-department webpages reveals that prison officials have plenty of security concerns about money transfers. It’s telling that when it comes to facilitating the flow of money into prison, many corrections departments are suddenly open to competition.

A map showing most people in prison only have one option for money transfers

It’s unclear how much competition actually benefits consumers

We took a closer look at fees in states that offered more than one option, and found that those states had slightly lower money-transfer fees. For example, the 11 states with multiple options had an average fee of 16% for a $20 transfer, as opposed to an average of 20% in 26 states that issued monopoly contracts (see table 2). But this only tells a part of the story. In the states with more than one option, it can be extremely complicated for a consumer to figure out what the lowest-cost option is.

Table 2: Shows the lowest available online money-transfer fees in states that offered more than one option. When states had multiple vendors, we show the vendor with the lowest fee for $20 and $50 transfers. Each state name links to its policy.

* Amounts are rounded to the nearest whole percentage. This results in small discrepancies between the number in this column and the first map in this briefing.

State with link to policy Money-Transfer Vendor(s) Competition Lowest available fee ($20 deposit) Fee as percentage of amount transferred* Lowest available fee ($50 deposit) Fee as percentage of amount transferred

Alabama Access Corrections Monpoly $2.95 15% $5.95 12%

Arizona Securus (JPay), GTL, Keefe Competitive $0.95 5% $4.95 10%

Arkansas In-house solution powered by Information Network of Arkansas (https://ina.arkansas.gov/); Access Corrections Competitive $1.75 9% $2.75 6%

California Securus (JPay), GTL, Access Corrections Competitive $1.95 10% $5.95 12%

⇡

Show all states

⇣

Wyoming Access Corrections Monpoly $5.95 30% $5.95 12%

As an example of complexity that can arise from multiple options, consider the California Department of Corrections (which houses over 130,000 people). California contracts with all three of the dominant money-transfer vendors (JPay/Securus, GTL, and Access Corrections). JPay is significantly cheaper than the other companies if you want to send $20. But increase the amount the transfer to $50, and JPay is the most expensive option. Worse yet, the prison department’s webpage doesn’t show a chart of the different companies’ respective fees–so the only way a family member can figure out the different fee options is to create accounts with three different companies, initiate test transactions in each system, and then manually compare the different fees (or maybe hunt around vendor websites for a fee table buried in some non-obvious place). The complexity of the options is outlined in table 3. And keep in mind that this is only an example based on two different amounts–if you wanted to send $30, you’d have to perform another round of test transactions to figure out the cheapest option. This kind of opacity seems purposefully designed to prevent consumers from finding the most cost-effective option.

Table 3: Selecting the least expensive money-transfer service is incredibly complex In California, which has three vendors, JPay is the cheapest company to send $20, but the most expensive to send $50.

$20 transfer $50 transfer

Money-transfer vendor Fee Fee as percentage of amount transferred Fee Fee as percentage of amount transferred

Securus (JPay) $1.95 10% $7.95 16%

Access Corrections $3.50 18% $6.95 14%

GTL $3.95 20% $5.95 12%

Prisons don’t have to outsource

Most prison systems appear to have outsourced money transfers, but there are still some that handle these transactions in-house. Several states still process money-order payments sent through the mail. We also identified four states (Arkansas, Maine, Montana, and Texas) that accept online payments through a general-purpose state-operated online payment platform.

Interestingly, Arkansas recently added Access Corrections as an alternative to the state-operated payment platform. Access Corrections’ fees in Arkansas are 25¢ less than the fees for the state-operated system, and are by far the lowest fees we have seen Access Corrections charge in any prison system–thus suggesting that companies set rates based on what other options are available, and they can provide low-cost transfers when they’re forced to.

Mailed payments are still an option in many states

The vast majority of states (around 45) still allow people to mail a money order at no fee. Some states direct people to mail those money orders to the department of corrections’ accounting office; other states outsource the processing to vendors like JPay and Access Corrections. But, just because there’s no fee, doesn’t mean there’s no cost–between the cost of the money order itself, and a stamp, the sender will probably pay around $2, but that’s lower than most online fees. The issue, of course, is speed. The vendors that hold correctional banking contracts earn their profits from fees charged for payments made online or over the phone. Do we trust them to promptly process money orders for which they receive no fee revenue? If their terms of service are any indication, the companies seem to reserve the right to deliberately delay money-order processing.

Don’t forget the fine print

People can’t use these money-transfer services without agreeing to fine-print provisions (sometimes called “terms of use” or “terms and conditions”). These take-it-or-leave it documents (known to lawyers as contracts of adhesion) are ubiquitous in modern life, but they take on a particularly sinister role in the context of prison money transfers. We all agree to boilerplate terms when we use services like Gmail, Netflix, or Amazon. Even though these giant corporations have the upper hand, there is a faint form of accountability: consumer advocates and journalists routinely scour terms and conditions for unfair surprises; when a particularly egregious term is exposed, companies can be shamed and consumers can “vote with their feet” by switching to other providers. None of these safeguards are applicable to correctional money-transfer services, where the company controls a critical service for incarcerated people.

Terms imposed by the dominant money-transfer vendors are replete with objectionable, misleading, and unfair provisions. We’ve grouped some of the more problematic provisions into five categories, discussed below.

1. Failure to promise anything in return for consumer’s money. Read a money-transfer website, and you’ll understandably be left with the impression that you can pay the vendor a fee to transfer money to someone in prison. But read the fine print, it turns out the companies don’t actually promise to do anything. All three of the leading companies disclaim “any warranty of any kind, express or implied.” Advertising a certain service (like transferring money) and then using fine print to disclaim any responsibility to actually provide that service is considered a deceptive practice under many consumer-protection laws.

2. Companies seem to go out of their way to make money-order payments arduously slow and plagued by uncertainty.

Seemingly intentional degradation of money-order payments. As noted above, sending a money order is obviously slower than making an online transfer, but in many cases it can be cheaper. But companies seem to go out of their way to make money-order payments arduously slow and plagued by uncertainty. JPay’s terms, for example, promise that payments will be “transmitted” within 1 or 2 business days, except for money-orders, which “are generally processed within ten (10) business days” (most people would refer to 10 business days as two weeks, which is an inexcusably long amount of time for processing small-dollar consumer payments). Both JPay and Access Corrections disclaim any liability for money orders that they receive, but which are not credited to the recipient’s account.

3. Privacy and consumer rights. Companies’ terms of use and privacy policies are replete with confusing or troublesome provisions regarding use of customers’ data. Some examples:

*JPay requires customers to consent to a credit check, which makes no sense because JPay does not extend credit and it’s unclear why the company needs that kind of private information.

*Companies say that user information can be shared with law enforcement, which at first glance isn’t terribly surprising. But many customers might be surprised that the terms of information sharing are so broad that they vitiate any kind of reasonable safeguards for consumers. Access Corrections, for example, says that it can share information with law enforcement, but it defines law enforcement as “personnel involved in the…investigative (public and private) or public safety purposes” (which, aside from being atrocious grammar, essentially means they can share your information with anyone who says they have a public safety purpose). GTL allows personal information to be shared with “law enforcement or correctional staff,” but doesn’t require that such staff have a proper job-related purpose for receiving such information.

*Access Corrections states that it has the right to use any customer communications to market its services, without notice or compensation to the customer. (Consumer activists successfully sued Facebook in 2011 for using customer likenesses without consent, but Access Corrections is apparently unconcerned about running afoul of the same laws that tripped up the behemoth Facebook).

4. Poorly designed services. Several miscellaneous provisions indicate how poorly these companies carry out their operations. For example, JPay terms state that the only cost to send money is the “service fee” that must be paid prior to making the transfer. But a different paragraph in JPay’s terms state that if the company owes money to a customer (e.g., for a refund), and the customer does not claim the money, JPay will eat up the amount of the refund by levying a “monthly service fee” (this monthly fee is not mentioned on any of JPay’s fee disclosure pages, nor do the terms of service specify how much the fee is). JPay also requires 2 weeks’ advance notice before cancelling a recurring payment (this is probably not allowed under Visa’s rules, which reference a 7-day maximum advance notice requirement and require a “simple” mechanism for cancelling recurring payments).

Dispute resolution. A lot of us are forced to agree to arbitration provisions buried in the fine print of consumer contracts. But these clauses, which prevent consumers from going to court to vindicate their legal rights, are especially troublesome when the company imposing the provision has a monopoly on an essential service. GTL allows customers to “opt out” of arbitration, but also states that the company can terminate the accounts of customers who exercise that right. JailATM, meanwhile, requires customers to consent to arbitration conducted by the National Arbitration Forum, a disgraced company that was forced to stop conducting consumer arbitrations in 2009 as part of a legal settlement (in fact, we pointed out this problem in our 2016 report on electronic messaging, but JailATM apparently has not bothered to update their terms in the intervening five years). Other troublesome terms that are unrelated to arbitration include one-sided indemnification provisions and limitations periods for disputes that are substantially shorter than most states’ statutes of limitations for contract claims.

Suggestions for improvements

The current system is complicated, inconvenient, and expensive. Different people have different opportunities to address these problems, as explained below.

Family members of incarcerated people

It may seem like family members have no leverage in this unfair system, but there are some things they can do to advocate for change.

*Complain about high fees or poor service. The Consumer Financial Protection Bureau (“CFPB”) has an easy-to-use online complaint system specifically designed for financial services like money transfers. Your state attorney general may also be able to investigate certain abusive or deceptive practices. If the relevant prison system has an ombuds or office of family support, send a copy of your complaint to them as well.

*Talk to legislators. Money-transfer vendors take advantage of the lack of regulatory oversight. It turns out that money-transfer vendors are subject to regulation in nearly all states as “money-transmitters;” however, money-transmitter regulations are focused on the fiscal health of the business (known as “prudential regulation”), not protecting consumers. But legislatures can close this loophole. Tell state legislators (or, in the case of jails, county commissioners) about the economic toll of money-transfer fees, and ask them to pass legislation requiring regulatory agencies to enact rules protecting customers of correctional money-transfer services.

*If possible, plan ahead and send a money order to avoid fees. If there are problems with money orders (slow processing, out of state mailing addresses), tell facility management and point out that “just send money online” isn’t an adequate response, because the online option is so expensive.

Regulators

*Federal law prohibits financial service providers from taking unreasonable advantage of a consumer’s inability to protect their own interests in selecting or using a consumer financial service. Users of correctional money-transfer services are unable to protect their own interests because they must either use a monopoly provider selected by a correctional facility, or choose from 2 or 3 options, all of which appear to set exorbitant prices in relation to their competitors. The CFPB is tasked with enforcing this law, and it should use its investigative and enforcement powers to crack down on unreasonably high money-transfer fees.

*The Federal Trade Commission (“FTC”) is also empowered to issue rules prohibiting specific unfair trade practices that cause reasonably foreseeable injury to consumers. The FTC should use this authority, either by itself or in conjunction with the CFPB, to develop rules governing maximum allowable fees and what types of contractual terms vendors can (or can’t) impose on customers.

Prison procurement officials

*At least part of the high cost of money transfers comes from some prison systems demanding or accepting “commissions” (or kickbacks) from vendors. As with phone contracts, prisons can help lower costs by refusing commissions.

*Look for in-house alternatives from other parts of state government. Prison systems are departments within state governments. Other state agencies are accustomed to accepting online payments (for vehicle registrations, hunting licenses, tuition, or any number of purposes). Have any of them developed low-cost in-house solutions for processing these payments? And if so, can those solutions be adapted for use in prisons? Arkansas, Maine, Montana, and Texas have figured out how to do it–other states should follow suit.

*Sending a money order by mail is a no-fee option in most states, but the utility of this option is severely limited when vendors deliberately prolong the amount of time it takes to process money orders. States can make this better in a number of ways. If at all possible, keep the processing of money orders in-house. If money-order processing is outsourced, there are two requirements that the state should put into its contract with the money-transfer vendor. First, the vendor should be required to process money orders within one business day of delivery. Second, the vendor should provide an in-state mailing address for all money order payments.

*Post all fees on the DOC information page: as noted above, some states sign contracts with multiple vendors, but don’t post the companies’ respective fees in one location. Every DOC webpage about money transfers should include an easy-to-read disclosure of applicable fees so that all family members and all staff members are aware of these fees.

*Provide specific details about garnishments/mandatory deductions. Many prison systems deduct money from incoming transfers to pay for mandatory fines, child support, restitution, cost of confinement, or other fees. Money-transfer vendors, unsurprisingly, disclaim any liability for these deductions. It’s true that these deductions are created by the state, so the state bears responsibility for explaining them. This is important information: if someone in prison needs $20 to pay for hygiene items, then a relative sending money needs to know how much to send so that the recipient actually gets $20 after mandatory deductions. Any webpage that includes information on how to send money should also include detailed information on how much is deducted and what deposits are subject to garnishment. This information should include what deductions apply to everyone, versus which deductions (like child support) only apply to a subset of recipients. Ideally, the webpage should also include a calculator so that users can type in a transfer amount and instantly see how much will be delivered to the recipient.

Companies

Last but not least, money-transfer vendors themselves have the most power to address problems in the industry they have created. While it’s probably unrealistic to expect these companies to voluntarily reduce fees, if companies are serious about their marketing puffery, there are other simple steps they could take to make customers’ lives easier.

*If companies are serious about their marketing puffery, there are other simple steps they could take to make customers' lives easier.

To the extent that money-transfer fees are inflated in part due to commissions being paid to correctional facilities, vendors should offer a commission-free alternative in all bids.

*All vendors include vague provisions in their terms of use that transfers from a customer’s credit card “may” be treated as a cash advance. While the vendor probably can’t give a definitive answer (because the bank or entity that issues the credit card the consumer is using has some discretion in how to handle these transactions), the vendors are the ones who create the transaction record, so they know how it’s coded. Vendors should provide customers with the precise transaction coding applicable to their payment so that customers can then be fully informed when they ask their own bank how the transaction will be treated.

*It costs very little to write fair and easy-to-understand contracts. Vendors should rewrite their terms and conditions and eliminate things like arbitration provisions, 2-week processing times for mailed payments, and disclaimers of any warranties whatsoever.

Footnotes

The term “trust account” is a term of art in the correctional sector, referring to a pooled bank account that holds funds for incarcerated people whose individual balances are sometimes treated as subaccounts. The term “trust” is used because the correctional facility typically holds the account as trustee, for the benefit of the individual beneficiaries (or subaccount holders). ↩

Paypal’s free transfers are available only for payments made from bank accounts; Paypal charges 30¢ plus 2.9% for a transfer coming from either a credit- or debit-card. CashApp doesn’t publish its fees, but others report that their fees mirror Venmo’s. ↩

We say “at least” eleven states because of the confusing role of companies like Western Union and MoneyGram. Many states list Western Union, MoneyGram, or a similar money services business, as one of several options for sending money, but that doesn’t mean there is true competition. For example, a prison system could contract with JPay to handle all money transfers, and JPay could subcontract with Western Union to handle in-person cash payments. The prison’s webpage may say that people can choose between JPay’s website and sending cash at any Western Union location, but in this hypothetical, Western Union is acting as an agent of JPay, not a competitor. Based on a variety of factors, we think that Western Union is an independent, competitive option for sending money to people incarcerated in Colorado, Connecticut, Illinois, Iowa and Washington’s prison systems. There may be other states where Western Union or a similar company is an actual competitive option, but it is very difficult to tell based on publicly-available information. ↩

Specifically, prison officials tend to spend a lot of time worrying about laundered or otherwise illegitimate money being sent to incarcerated people. It’s not that these concerns are never valid, but we do wonder how prevalent the problem actually is. The latest major example of this narrative occurred in June, when the Washington Post, possibly acting on a leak from the federal Bureau of Prisons, published a story claiming that “there are more than 20 [federal] inmate accounts holding more than $100,000 each for a total exceeding $3 million.” This makes it sound like nefarious trust-account activity is some kind of huge problem, but if there is a problem the BOP has all the tools it needs to investigate suspicious transactions and take corrective action. More importantly, the same article notes that there are roughly 129,000 people incarcerated in BOP facilities, and the total balance of all trust accounts is somewhere around $100 million. If you subtract the $3 million in the 20 high-balance accounts, you arrive at an average account balance of $752 (i.e., $97 million divided by 128,980 people). That’s hardly a lavish amount of money (and keep in mind it’s a mean average, so it probably skews high due to a comparatively small number of people whose trust accounts receive pension or other income payments). ↩

The cost difference was narrower for a $50 transfer, with an average fee of 11% for states with multiple options, versus 13% in monopoly states. ↩

The U.S. Postal Service charges $1.45 for a money order (up to $500 face value), Walmart charges up to $1. A first-class stamp is currently 58¢. ↩

JPay “Payments Terms of Service” P 17 (dated Aug. 18, 2021; accessed Oct. 19, 2021); GTL “Terms of Use” P 16 (dated Jun. 25, 2021; accessed Oct. 25, 2021); Access Corrections “Terms & Conditions” at paragraph titled “Disclaimer of Warranties and Limitation of Liability” (dated Aug. 23, 2021; accessed Oct. 19, 2021). ↩

JPay “Terms of Service” P 6 (emphasis added). ↩

JPay “Terms of Service” P 7; Access Corrections “Terms & Conditions” at paragraph titled “Money Orders.” ↩

Aventiv Technologies, “Privacy and Data Processing Policy,” paragraph entitled “Business purposes for the collection of personal information (dated May 5, 2021; accessed Oct. 19, 2021) (Aventiv is the parent company of Securus and JPay). ↩

Access Corrections, “User Agreement,” paragraph entitled “Agency Access” (dated Mar. 19, 2009, accessed Oct. 19, 2021). ↩

GTL “Terms of Use” P 6. ↩

Access Corrections “Terms & Conditions” at paragraph titled “Use of information submitted.” ↩

JPay “Terms of Service” PP 5 and 9. ↩

JPay “Terms of Service” P 13. ↩

Visa Core Rules and Product & Service Rules S 5.8.10.1, tbl. 5-18 (Oct. 16, 2021). ↩

GTL “Terms of Use” P 22(d). ↩

JailATM, “Terms of Agreement,” paragraph titled “Governing Law” (undated, accessed Oct. 25, 2021) ↩

JPay “Terms of Service” P 16; Access Corrections “Terms & Conditions” at paragraph titled “Indemnity.” ↩

JPay and Access Corrections both require that claims be filed within one year of the claim arising. JPay “Terms of Service” P 15; Access Corrections, “User Agreement,” paragraph entitled “Disputes.” JPay’s provision is especially tricky because it defines the time limit as 12 months from the customer’s “constructive knowledge” of the claim, without defining the term “constructive knowledge” (lawyers can, and have, argued for years about the meaning of constructive knowledge, so expecting consumers to understand the term is unrealistic), and because JPay requires customers to give the company 30 days’ notice before filing a claim, which effectively shortens the limitations period from 1 year to 11 months. ↩

Dodd Frank Wall Street Reform and Consumer Protection Act, Pub. L. 111-203 SS 1031(d)(2)(B) and 1036(a)(1)(B) (Jul. 21, 2010)(codified as 12 U.S.C. SS 5531(d)(2)(B) and 5536(a)(1)(B)). ↩

15 U.S.C. S 45 (a)(1) and (4). ↩

The issue of mailing distance has recently assumed heightened importance as the U.S. Postal Service has implemented a plan to slow down the mail, particularly mail traveling long distances. For example, even under the new mail-delivery standards, mail sent in Minnesota should reach most prisons in the state within two days. But if someone in Minnesota wants to send a money order to someone in the Minnesota prison system, it has to be mailed to JPay’s office in Florida, which takes twice as long. States can mitigate against this unreasonable delay by prohibiting vendors from using out-of-state addresses for receipt of money orders. ↩

JPay’s parent company, for example, brags that it “delivers superior value and service to all of our customers nationwide” (see Aventiv Technologies, “Privacy and Data Processing Policy,” introductory paragraph), a claim that’s hard to square with its actual pricing and user contracts. ↩

Some card networks don’t even use the term “cash advance.” Visa rules, for example, use the terms “account funding transactions” and “manual cash disbursement,” which describe two mutually exclusive type of cash-like transactions. ↩

Stephen Raher is the General Counsel at the Prison Policy Initiative. (Other articles | Full bio | Contact) Tiana Herring is a Research Associate at the Prison Policy Initiative. (Other articles | Full bio | Contact)

Other posts by this author

|

2023 may 31

|

2023 mar 20

|

2022 aug 23

|

2022 aug 23

|

2022 aug 23

|

2022 aug 23

|

More... |

Subscribe

Get notifications when new letters or replies are posted!

| Posts by Charles Douglas Owens, II: |

|

email me |

|---|---|---|

| Comments on “Show me the money: Tracking the companies that have a lock on sending funds to incarcerated people”: |

|

email me |

| Featured posts: |

|

email me |

| All Between the Bars posts: |

|

Replies (1)

I am following the steps you outline in this article concerning, "what can I do?" This is a disgusting greedy money grab and after the money is so heavily taxed the state sells commissary goods overpriced, and provides substandard necessities to those who cannot pay for the overpriced goods. The burden falls squarely on family and friends of the incarcerated, and of course on those guys and gals who desperately need the necessities sold as exorbitant prices. Regulation of the entire industry is called for. All states participate in this travesty by way of monopoly and by kickbacks through contract conditions. My heart goes out to all those who suffer from the greed of corrupt America and the greed of county, state, and federal authorities and staff. Thank you for this article when properly considered, will lead the compassionate reader to outrage, and in hope, to action as outlined in the article.

I remain, John

March 2, 2022